Money market Photo Credit: ALAMY/VI CONSORTIUM

In a 8-6 vote, senators of the 33rd Legislature on Thursday night approved Governor Albert Bryan's debt refinancing plan, even as all expressed concerns with the measure, but with those who supported it stating that there was nothing better on the table and that the risk is worth it.

The deal creates a special purpose vehicle and gives control of the Internal Revenue Matching Fund to the SPV in an effort to win a favorable credit rating to shop the bond market — something the local government has been unable to do with its junk-status credit rating. According to testifiers, the deal has received a BBB bond rating by the Kroll Bond Rating Agency.

Voting Yes: Allison DeGazon, Donna Frett-Gregory, Alicia Barnes, Myron Jackson, Stedmann Hodge, Athneil Thomas, Steven Payne, and Marvin Blyden.

Voting No: Kurt Vialet, Janelle Sarauw, Javan James, Kenneth Gittens, Dwayne DeGraff and Okland Benta.

Senate President Novelle Francis was absent and is off island dealing with a family medical emergency.

The contentious hearing spanned all Thursday, as senators went back on forth on the controversial bill. Virtually all expressed reservations, and at one point — going based on testimony of lawmakers and concerns expressed — it appeared that the measure would fail.

One example is the fact that the Bryan administration called for lawmakers to ratify the agreement even though the rum companies' contract had been changed and there were no representatives of the rum companies at the hearing to answer questions. In fact, changes the administration had negotiated with Diageo were not completed and signed until late Thursday. When it was finally executed, the agreement was quickly forwarded to the Office of the Senate President, giving little time for lawmakers to vet the agreement.

The senators expressed concern, but they signed on anyway.

They also expressed concern with the structure of the measure, but they signed on nonetheless.

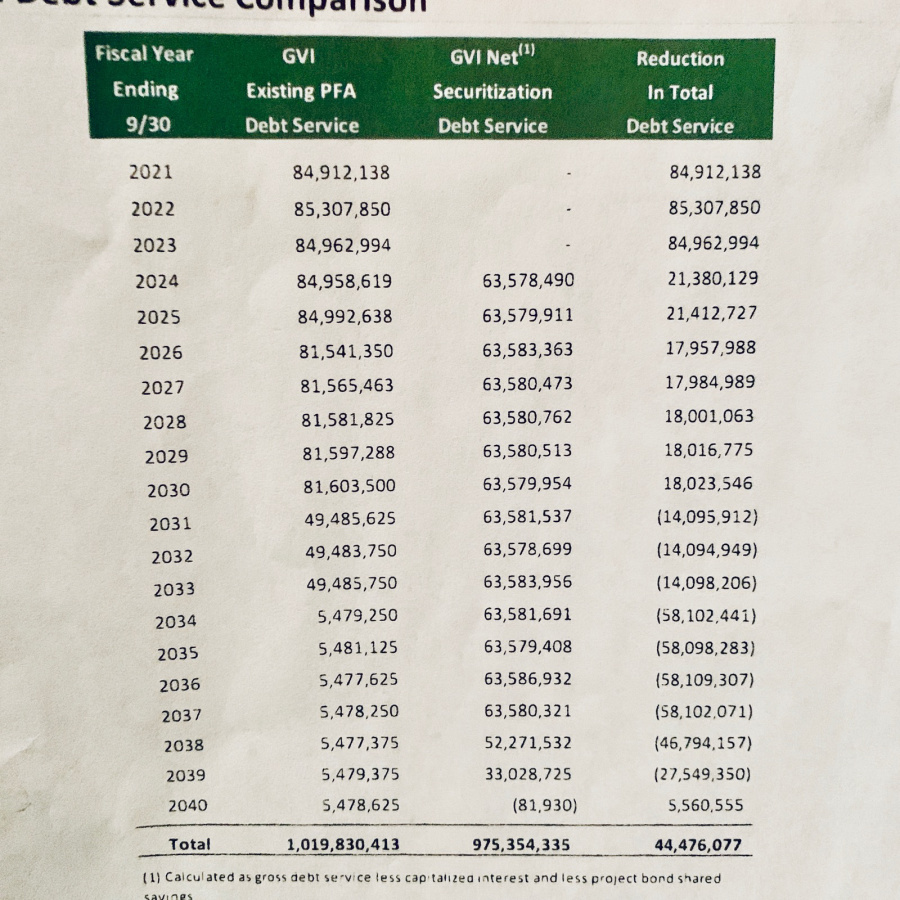

A chart showing the plan's structure. Dissavings, beginning in year 2031, are seen in parenthesis on the right side of the chart. (Courtesy: V.I. Legislature)

The bill gives Governor Bryan the authority to enter into a 20-year contract to refinance the territory's Internal Revenue Matching Fund, or rum cover-over funds, in what the administration says will yield a lower interest rate and allow the government to re-enter the bond market. In the first three years, the agreement would see the government receiving $85 million, $150 million of which will be monies from the territory's Debt Service Reserve Fund that was part of a fail-safe system, called a lockbox, that previously could have only been used to pay the territory's obligations if, for example, a calamity were to strike and affect the territory's normal means of meeting its debt obligations.

The new agreement dismantles this structure and uses the funds as part of the $85 million a year in payments to the territory.

Another concern was the ballooning effect of the bill, with some senators describing the contract as predatory. According to the agreement, in the first three years, the government pays no debt service, which explains why the $85 million is possible every year for three years. But the agreement sees payments escalating from year 10, with the government seeing hundreds of millions of dollars in dissavings thereafter. And for an agreement that refinances over $1 billion of the territory's debt, the savings for its lifetime of 20 years amounts to only $44 million. This fact gave lawmakers pause as well.

Under the current setup, the territory would be paying $5 million in debt service payments in 2034, according to Mr. Vialet. Instead, under the new plan, the USVI will be paying $63 million while seeing dissavings of $58.1 million in the same year. In fact, according to a chart provided by the administration, dissavings in the last ten years of the agreement totals $297 million.

"The deal is structurally wrong," said Mr. Vialet. "The dissavings in the last ten years is $300 million. What they're doing now is they are paying zero debt service this year, next year and the year after and it passes on to the latter years."

In essence, during Governor Bryan's remaining first term in office, the territory pays no debt service while receiving $85 million every year for the next three years for a total of $255 million, according to the chart. Thereafter, beginning in 2034 until 2039, the structure sees the escalation of dissavings from $14 million to $63 million for a total of roughly $297 million in dissavings. All this even as the government makes annual debt service payments from 2024 to 2039 amounting to roughly $1 billion.

"I'm sorely disappointed because the deal is not favored in the best interest of the Virgin Islands," said Mr. Vialet. "We're going to feel it just like we're feeling the effects of the Diageo deal right now, where we're making good money but we have to give them half of it."

"Today was party over people," said Ms. Sarauw, arguing that lawmakers who supported the measure forsook better judgement to support the Democratic Party's need to see the measure approved. "If you listen to the line of questioning by all of my colleagues, everyone today had an issue with that bill. We went into lengthy recesses because there were grave issues with the bill."

An amendment moved by Mr. Blyden called for the deal to be executed by Sept. 30 or the entire law is rendered null. It also sets the maximum interest the government could accept to 3.7 percent.

Supporters of the measure, though they expressed concerns, said they saw no other choice. Some said it was a risk they were willing to take.

"I wonder do we frown on bills because it's not our idea, or do we frown on bills truly out of research and believing wholly that it is, in fact, not a good idea," said Ms. DeGazon as she verbalized her strong support for the measure.

"... We have to really weigh in the balance what is before us, the implications, and at the same time look towards making the government of the Virgin Islands investment-worthy once again," said Ms. Barnes.

Mr. Payne said he supported the measure because of the possible funding it provides for G.E.R.S.; Mr. Jackson and the other lawmakers who supported the bill also cited the pension system as their main reason to vote Yes. G.E.R.S. has said if it does not receive a $195 million immediate infusion of cash, it would be forced — with Senate approval — to cut retirees annuities by 42 percent.

Also approved as part of the bill was the rum cover-over funds being sent by the U.S. Treasury to what has been named a "Restricted Account" owned by the government of the Virgin Islands. Previously the U.S. Treasury would have to send the funds to the special purpose vehicle. However, under the revised bill the funds go directly to the Restricted Account whose sole responsibility is to remit those funds to the special purpose vehicle within one day. Those changes had to be made because the U.S. Treasury would not remit the monies to no other entity except the government of the USVI, effectively removing itself from the deal.

Senator Donna Frett-Gregory, who up until the end sounded as if she would have voted against the measure, at the last minute voted in favor and essentially became the deciding factor. Asked about it during an interview following the vote, she said, "While it's not a perfect situation, what is important for us to note is that we've sat in the Legislature for the past 19 months, and I've spoken to my colleagues about us addressing G.E.R.S., but we really haven't in the meaningful way that we should have."

Advertisements