Governor Albert Bryan on Tues. Feb. 8th 2022 signed a bill into law that allows the V.I. gov't to refinance rum cover-over bonds, officially called the Internal Revenue Matching Fund Bonds, to fund GERS for 30 years. Photo Credit: GOV'T HOUSE

Just over a week after it was approved by the 34th Legislature, Governor Albert Bryan on Tuesday signed into law a bill allowing the V.I. government to seek funding in the bond market to undergird the Government Employees' Retirement System for 30 years.

Flanked by administration officials, lawmakers and others, the governor signed Bill No. 34-0188 into law at Gov't House in St. Thomas — the first action to be taken at the historic building since it was ravaged by Hurricanes Irma and Maria in 2017, Government House said.

“When we first introduced this concept to create a special purpose vehicle corporation to refinance our rum bonds 18 months ago, we did it with the people in mind. We did it to protect the pension benefits of our almost 9,000 government retirees and with the goal of protecting the pensions of the more than 8,000 other active employees who are relying on the Government Employees Retirement System to be able to achieve a decent quality of life in retirement,” Governor Bryan said before signing the measure into law, according to a release issued by Gov't House.

He added, “Today is about them: The retirees who are the breadwinners in their respective households and who rely on their pension benefits to provide for their families; the retirees confronting inflation and the rising cost of goods, and whose pension benefits are their only source of income. We did it to protect the pensions of the active, vested employees so they too can realize the promise of benefit funds when they retire."

Bill No. 34-0188 allows the V.I. Public Finance Authority to create a new entity called the “Internal Revenue Matching Fund (IRMF) Special Purpose Securitization Corporation,” which will be a legally created entity separate from the government. The IRMF gets is funding from taxes collected from the sale of rum produced in the U.S. Virgin Islands and sold in the United States. The government usually collects an estimated $250 million annually, delivered in September. A bulk of the IRMF funds are already set aside to pay the territory's debt obligations. In the new agreement, the IRMF would be refinanced and its funds managed by the special purpose corporation.

Here's how David Paul, head of Fiscal Strategies Group, Inc. and financial advisor to the P.F.A., through which the transaction is being managed, explained the deal: "The PFA does not have the ability to separate itself from the government's credit rating the way it did in the late 1980s. So we're creating a special purpose financing corporation — you could call it PFA2 so that it has less of a mysterious name — simply to provide a way of securing the Matching Fund revenues in a way that you can do the best possible financing without the rating of the government being attached to it, and without being penalized for the fact that the government financial statements are not yet timely enough to allow a full public underwriting. So it's really a way of simply building public confidence so that you can do a better, lower-cost financing, and the lower the cost of financing, the more money we're able to direct to the GERS."

Mr. Paul also likened at least portion of the new agreement to the refinancing of a home to realize savings that the homeowner could use for other priorities.

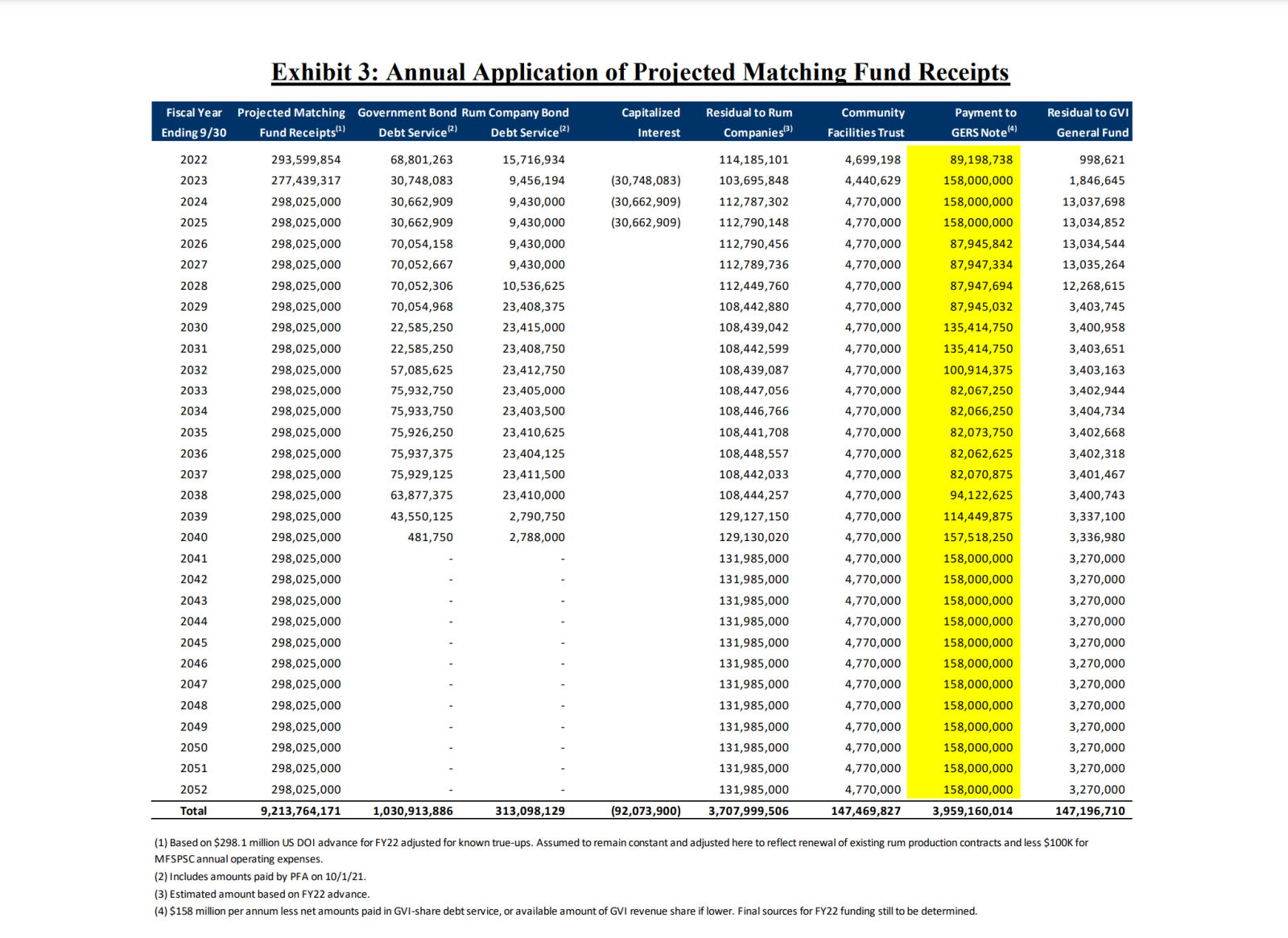

If the government is successful on the bond market in its refinancing and restructuring bid, G.E.R.S. would receive $90 million in the first year, then $158 million for the following three years. The payments to the pension system average $131 million for the 30-year duration of the contract, with payments fluctuating between $82 million at its lowest and $158 million at the highest, according to a chart provided by the government, seen below.

The payments to G.E.R.S. will be made every September. Mr. Paul said the PFA would like to go to market early March. PFA Director of Administration and Finance, Nathan Simmonds told Ms. Frett-Gregory that there was "tremendous appetite" for Virgin Islands bonds, meaning he expects that the government will be successful in securing the refinancing and restructuring deal.

As part of the agreement, G.E.R.S. will dismiss its case against the government for the remaining $19 million that the pension system says it is owed for employee and employer contributions. However, the agreement does not address $4 billion in actuarially determined employer contribution, or ADEC, that G.E.R.S. also contends it is owed. Though G.E.R.S. stands to receive more than $4 billion in payments over the 30-year period as part of the new agreement, the pension system's administrator, Austin Nibbs, maintains that unless the funds are fully paid, the ADEC court matter would remain active.

The measure, now law, was Mr. Bryan's fourth attempt to buttress G.E.R.S. after a third effort failed when it was rejected by the Senate in December 2020. Lawmakers had said the measure was not in the best interest of the territory; some contended that the refinancing, contrary to what was being said, was not certain to go toward saving G.E.R.S., while others, including Finance Committee Chairman Sen. Kurt Vialet, contended that the deal would affect future generations as it would have deferred payments and place a heavy burden on Virgin Islanders ten years down the road.

The bill Mr. Bryan signed into law Tuesday is vastly different from the measure deliberated in 2020, according to Mr. Paul, head of Fiscal Strategies Group, Inc. and financial advisor to the P.F.A. "There's really night and day differences," he said on Jan. 31. "The prior legislation was about a refunding for savings, which is certainly an admirable thing, and it provided some liquidity to some funds to G.E.R.S. But working with the administration folks, and with members of the Senate and with GERS and their actuary, our entire purpose here was fundamentally different. The restructuring is a tool, but it's a tool with a much larger objective which is long-term solvency for GERS. That is the defining purpose of this legislation."

On Jan. 31, senators praised the new deal — forged through a number of meetings between G.E.R.S., Gov't House, and critically a G.E.R.S. Senate subcommittee created by Senate President Donna Frett-Gregory and chaired by Mr. Vialet. Other members of the committee include Sens. Dwayne DeGraff, Milton Potter, Carla Joseph and Novelle Francis.

"All ye that labor and a heavy laden, rest assured that there's help on the way," said Mr. Francis as he hailed the passage of the measure in the Senate on Jan. 31.

Ms. Frett-Gregory stated, "The time is always right to do the right thing, and while this may not be perfect for some of us, it is important that you recognize that if you wait for perfect nothing will get done. The retirees and future retirees of the Virgin Islands can sleep easy tonight."

Mr. Vialet, the bill sponsor, thanked his colleagues for their support of the legislation, and spoke of a number of important items in the bill that he said came from the Senate — including $40 million from the IRMF to G.E.R.S. that was once allocated to the general fund of the local government. "So I don't want for this body to not recognize their contribution to this measure that we have before us today," he said.

"So the narrative can be what it wants, but at the end of the day the true narrative is that the 34th Legislature put a lot of time and effort to make this a reality, and as a result of the previous rejection, we are now here to discuss a 30-year annual funding to the Government Employees' Retirement System," Mr. Vialet concluded.

Advertisements